AkinovA is a secure, globally regulated, end-to-end electronic marketplace for the transfer and trading of insurance and reinsurance risk. AkinovA is the owner of the A1Policy, its wording and the technology that supports it.

AkinovA’s Bermuda subsidiary is regulated by the Bermuda Regulatory Authority under a novel regulatory framework and is the only successfully authorised entity to date. It is authorised to trade with brokers, insurers, reinsurers, ILS funds, capital market investors, listed corporates, data analytics and service providers in 41 countries. AkinovA Ltd. is FCA authorised (UK Appointed Representative as an intermediary for both Insurance and General Investments) and ISO27001 certified.

No, we are not a carrier. AkinovA is regulated as an Insurance Marketplace but neither as a broker nor as a carrier of insurance. As a result, AkinovA remains neutral, is already multi-broker, is regulated whilst it does not compete with its clients and ecosystem and is global.

No, we are not a broker. We are regulated as an insurance marketplace, but neither as a broker or a carrier. We remain neutral in any given transaction

No. AkinovA is not an MGA at this time although it is likely that an MGA will be required to provide MGA–style services on behalf of carriers in the medium term.

The data on AkinovA are owned and controlled by the parties who provide them (the client carriers and other advisors such as broker, actuaries).

Only AkinovA authorised personnel and people / entities authorised by the client have access to client data through AkinovA.

Yes, our technology is secure and ISO27001 compliant.

Yes, AkinovA Bermuda is licensed under Bermuda law to place multi-class, multi-year contracts in 41 countries.

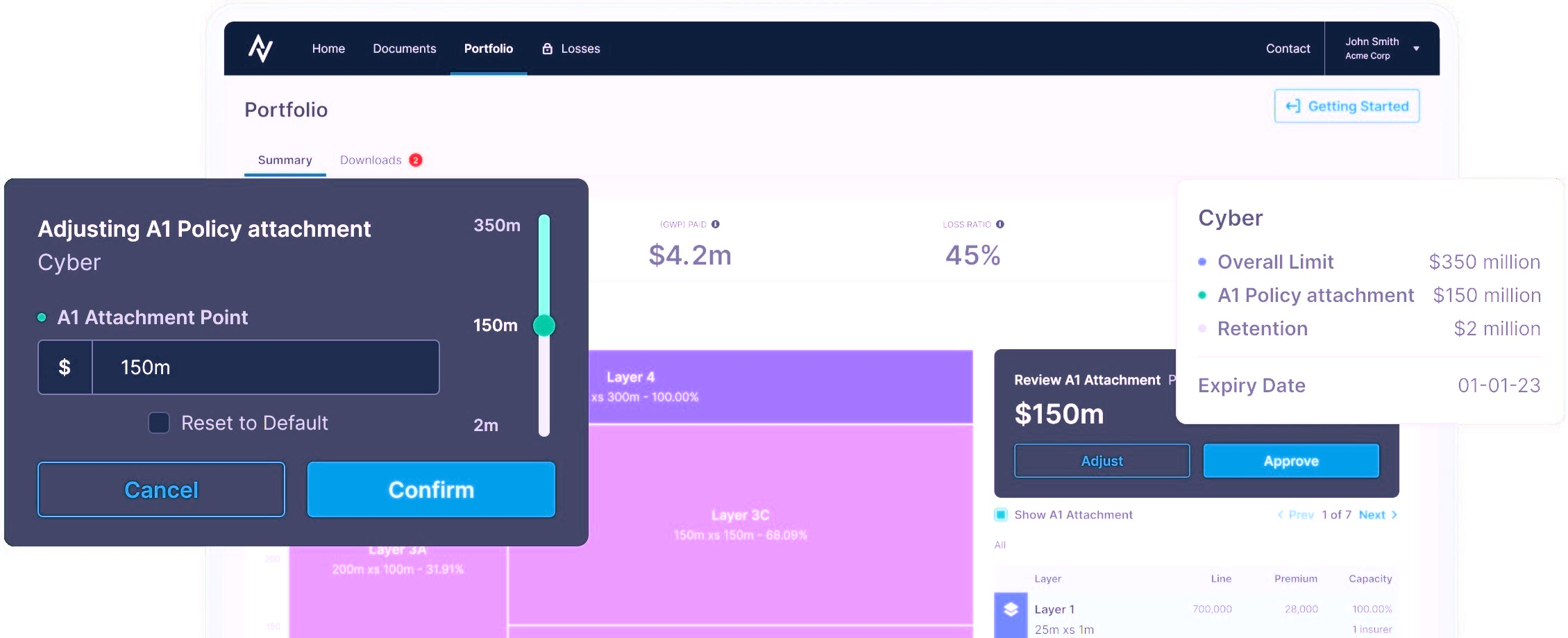

The A1Policy is a technology-enabled integrated insurance solution for Fortune 500-type companies providing excess [difference in limits] umbrella coverage across multiple lines of business. It is not only designed to transfer traditional insurance risk but also generate meaningful capital relief for both buyers and sellers. Simultaneously, A1Policies are packaged into baskets of risks and transformed into the capital markets thereby creating much needed new capacity to underwrite existing and new risks

Typically, this would entail the following steps:

Provision by the client or their representative of historical claims and exposure information (ideally at least the past 5 years) by class of business including EP curves / distributions and parameters followed by replication / validation of client ground-up stochastic model.

Inclusion within model of expiring / renewal programme with necessary parameters and assumptions for expenses / brokerage etc.

Inclusion of A1Policy options with necessary assumptions.

Comparison of structures using appropriate metrics and discussion.

If necessary, AkinovA can assist in the modelling of the risks.

The A1Policy wording is owned by AkinovA.

Yes. Our General Counsel will be delighted to walk you through the A1Policy wording when convenient.

The A1Policy wording is standardised to facilitate the ease of transfer of risk between buyer and seller / risk taker (carrier / capital markets) in addition to allowing AkinovA to bundle A1Policy contracts together into baskets of risk to better access capital markets capacity

There is no minimum ticket / line size though typically companies that most benefit from the A1Policy are those with a significant risk management function and / or have their own captive(s).

The data come direct from the proposing client or via their chosen Concierge Partner (see below).

As risk taker (carrier / capital market), you will receive data for all lines of business individually being considered. This is important as the A1Policy is an umbrella policy and therefore it will be necessary to allocate premium, claims and capital by line, not just on an aggregate basis.

The A1Policy, by design, is a whole account, multi-year contract providing annual coverage on an Each and Every Loss (EEL) and in the annual aggregate as this provides the maximum amount of diversification and hence cost and capital efficiency. However, the A1Policy app enables the corporate, its advisors and carriers to attach each LOB at different levels to match appetite and needs.

No, the A1Policy supplements and follows the terms of your existing coverages.

AkinovA provides preliminary risk analysis, underwriting and indicative pricing to determine the efficacy of the A1Policy relative to the current (re)insurance structure but it is ultimately the carrier that will perform its own due diligence and determine whether the risk / price is acceptable.

AkinovA does provide indicative pricing based on its own view of the risk but it is a process of negotiation between the buyer and the seller that will ultimately set the price.

The A1Policy is tailored to each individual client’s requirements regardless of the state of the market. Being a multi-class / multi-year policy, it is intended to smooth out the effects of volatilities in the insurance marketplace. This provides benefits to both buyer and seller so as to engender a longer-term relationship. The A1Policy process determines the efficacy of the A1 approach relative to the buyer’s and seller’s existing arrangements. Both sides are thus enabled to make the most informed decisions.

Your current insurance provider(s) / current broker will perform claims-handling advocacy services. AkinovA will respond excess of those arrangements. The lead carrier on the A1Policy and / or the MGA that originates and underwrites the business will handle claims that attach to the A1Policy (recognising that the underlying insurance programme will have its own embedded claims–handling protocols).

There is no need for collateral because there is a standard capital markets instrument with the usual chain of security implemented in full.

As part of our regulated functions, AkinovA can approach all forms of capacity on behalf of the client, including alternative capital.

Yes

Subject to local regulations, corporates and carriers can engage with AkinovA directly or via their broker.

The Integration Partner is a totally separate role to that of the Concierge Partner. The Integration Partner ensures all data flows are technologically enabled.